Understanding Estate Planning for Today’s Modern Families

Blended family estate planning requires specialized strategies to protect all family members. Here’s what you need to know:

- Definition: A family where at least one spouse has children from a previous relationship

- Key challenges: Balancing needs of current spouse and children from previous marriages

- Essential tools: Living trusts, QTIP trusts, proper beneficiary designations

- Without planning: Assets may unintentionally pass to ex-spouses or exclude stepchildren

- Best practice: Work with an attorney experienced in blended family situations

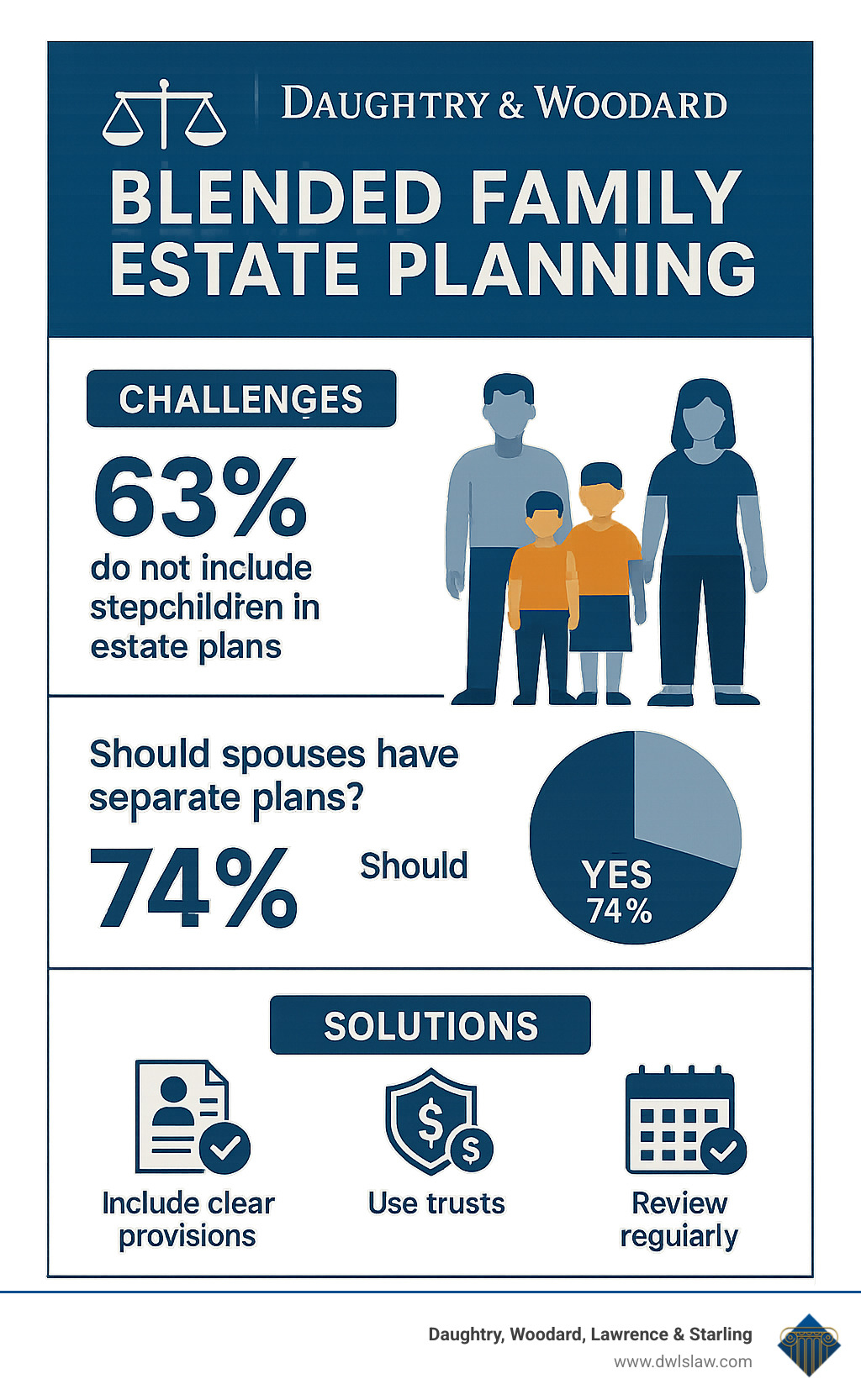

In America today, blended families represent 21% of all opposite-sex couples, with 63% of remarriages involving stepchildren. This modern family structure brings joy and fulfillment—but also creates unique estate planning challenges that traditional approaches don’t address.

Without proper planning, the death of a spouse can trigger family conflicts, unintended disinheritance, and costly probate proceedings. In California alone, probate on a $2 million estate can consume between $75,000 and $100,000 in fees.

The emotional dynamics in blended families make standard estate planning insufficient. When a parent remarries, questions arise: How do you provide for your current spouse while ensuring your biological children receive their inheritance? What happens to stepchildren who may have no legal inheritance rights? How can you prevent your hard-earned assets from being redirected away from your intended heirs?

The stakes are high. Without a custom estate plan, your spouse might inherit everything while your children wait decades for their share—or worse, receive nothing at all if your spouse later changes beneficiaries.

I’m Kelly K. Daughtry, an attorney at Daughtry, Woodard, Lawrence & Starling with extensive experience guiding North Carolina families through the complexities of blended family estate planning. Our firm has helped hundreds of blended families create customized plans that protect all loved ones while minimizing potential conflicts.

Blended family estate planning definitions:

– North Carolina probate attorney

– estate planning for couples

– estate planning for seniors

Blended Family Estate Planning: Why It’s Different

When two families join together, it creates something beautiful – but also something that requires special care when it comes to planning for the future. The numbers tell a compelling story: over 16% of children in America live in blended families, and 40% of marriages include at least one previously married spouse. This isn’t just a statistical footnote – it’s a significant shift in how American families are structured.

So why does blended family estate planning need a different approach? It comes down to a simple truth: traditional estate planning was designed for traditional families, but life is rarely that straightforward anymore.

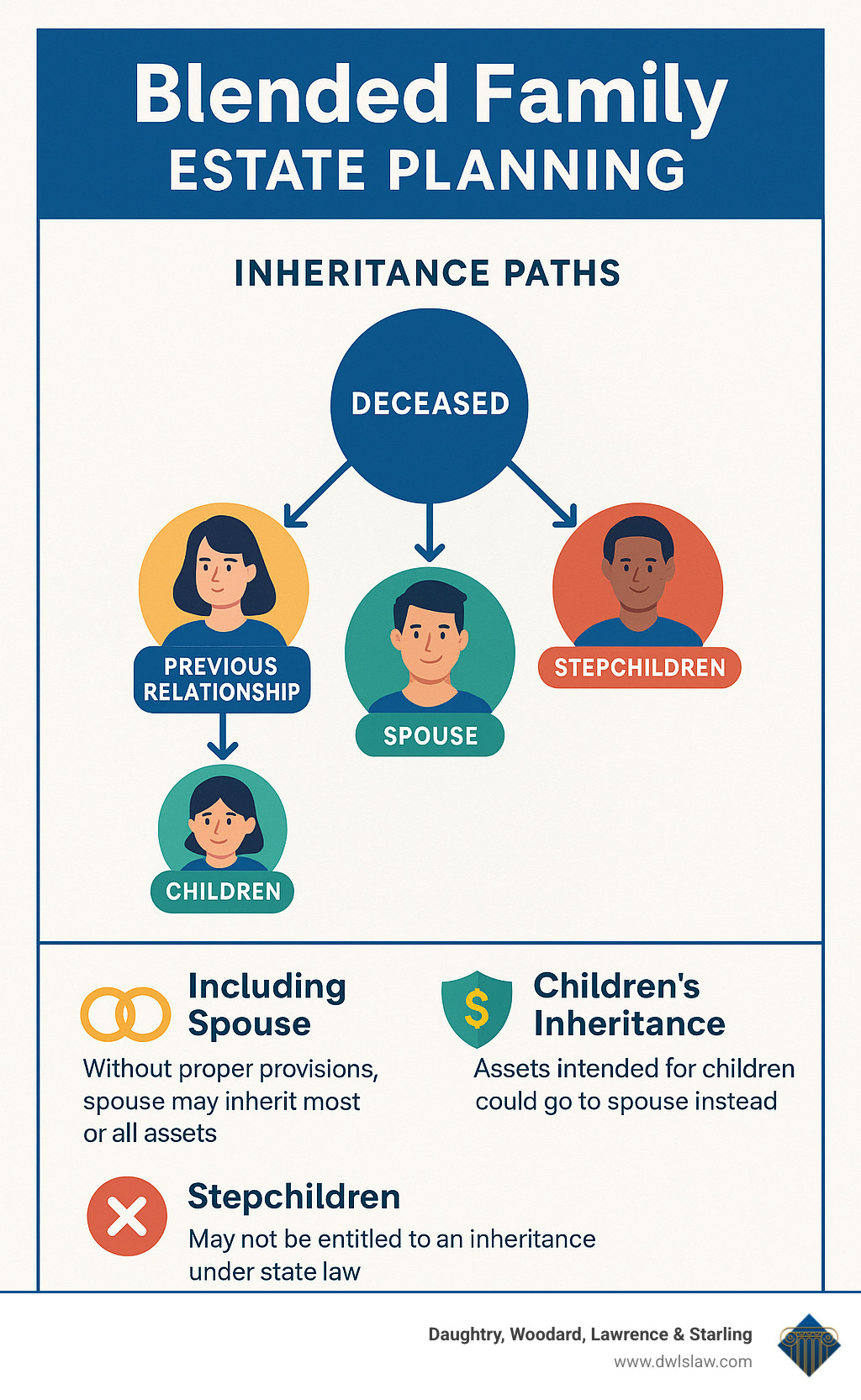

Without specialized planning, the legal system tends to create outcomes most blended families wouldn’t choose. Your current spouse might inherit everything while your biological children receive nothing. Or your stepchildren – who you love as your own – might be left out entirely because the law doesn’t recognize them as legal heirs.

As Pew Research has documented, American families have transformed dramatically in recent decades. Unfortunately, many estate laws still operate as if we’re living in the 1950s, creating a disconnect that can tear families apart when they’re already dealing with loss.

Common Pitfalls in Blended Family Estate Planning

I’ve seen the same heartbreaking scenarios play out repeatedly in my practice. A loving parent passes away, believing everything is taken care of, only for their family to find costly oversights:

Outdated documents remain one of the biggest problems we see. Life moves quickly – you remarry, form new relationships, welcome new children – but your will from 15 years ago still names your ex-spouse as beneficiary. This disconnect can create chaos at exactly the moment your family needs clarity.

Beneficiary designations are perhaps the most frequently overlooked aspect of estate planning. Your will might be perfect, but if your 401(k) still lists your former spouse as beneficiary, that money goes directly to them – regardless of what your will says. These designations trump everything else.

Joint ownership arrangements can inadvertently disinherit children. When you own property jointly with your new spouse, it automatically passes to them upon your death – potentially cutting out children from your previous marriage entirely.

AARP has highlighted how these planning oversights particularly damage the 16 percent of children in blended families. What starts as an oversight often ends as a family rift that never heals – precisely what most parents would give anything to prevent.

What Happens If You Die Intestate?

Dying without a will – what lawyers call dying intestate – means surrendering control to your state’s one-size-fits-all formula. And let me tell you, these formulas rarely align with what blended families would choose.

Here in North Carolina, intestacy laws create particular challenges for blended families:

If you pass away leaving both a spouse and children from a previous relationship, your spouse typically receives only a portion of your estate – often just one-third to one-half. The remainder goes to your biological children.

But here’s where it gets complicated: stepchildren receive absolutely nothing under intestacy laws unless you’ve legally adopted them. That teenager you’ve raised since they were five? The law sees them as a legal stranger to your estate.

The distinction between separate property (owned before marriage or received as gifts/inheritance) and community/marital property becomes critically important too, with different rules applying to each.

I’ve sat with too many grieving families who finded too late that the law’s default settings created financial hardship for surviving spouses while simultaneously breeding resentment among children who felt overlooked or forced to wait years for their inheritance.

The emotional and financial stakes are simply too high to leave your family’s future to intestacy laws. Blended family estate planning isn’t just about distributing assets – it’s about preserving relationships and honoring the unique bonds that make your blended family special.

Core Tools for a Peace-Proof Plan

Creating harmony in blended family estate planning requires specialized tools that balance competing needs and protect all family members. At Daughtry, Woodard, Lawrence & Starling, we help families steer these complexities with thoughtful solutions that bring peace of mind to everyone involved.

The right legal tools can make all the difference between a smooth transition and years of family conflict. While the upfront cost of creating comprehensive estate plans might seem significant, it pales in comparison to the emotional and financial costs of inadequate planning. It’s not just about distributing assets—it’s about preserving relationships and honoring your wishes.

Wills vs. Living Trusts for Blended Family Estate Planning

While wills serve as foundation documents, they often fall short for blended families. Think of a will as giving directions after you’ve left the party—important, but limited in scope.

A basic will goes through probate—a public, often expensive, and time-consuming court process. For blended families, this publicity can amplify tensions during an already emotional time. Wills also take effect only at death, offering no protection during incapacity, and they provide minimal control over how assets are distributed over time.

Living trusts, on the other hand, work more like having a trusted friend manage the party according to your detailed instructions. They avoid probate entirely, keeping your family’s financial matters private. They allow for nuanced distribution plans—perhaps providing income to your spouse while preserving principal for your children. As we explain in our guide on whether you should consider a trust for your estate plan, trusts offer flexibility that’s particularly valuable for ensuring children from previous marriages aren’t accidentally disinherited.

Living trusts also provide essential protection for your assets and loved ones by allowing you to specify exactly who inherits what, when, and under what conditions—giving you the control needed to honor all your family relationships.

QTIP & AB Trusts: Protecting Spouse and Kids

For blended families, specialized trusts offer solutions to the “either/or” dilemma of providing for both spouse and children.

A QTIP Trust (Qualified Terminable Interest Property Trust) works like a lifetime income stream for your spouse with a guaranteed inheritance for your children. Your spouse receives all income from the trust assets for life, enjoying financial security and comfort. Meanwhile, the principal remains protected for your chosen beneficiaries—typically children from a previous marriage. This arrangement qualifies for the unlimited marital deduction, deferring estate taxes until your spouse’s death while preventing your spouse from redirecting assets away from your chosen heirs.

The AB Trust (sometimes called a Bypass Trust) takes a different approach by splitting assets into two trusts when you pass away. Trust A (the Marital Trust) provides for your spouse, while Trust B (the Bypass Trust) preserves assets for your ultimate beneficiaries. This structure not only maximizes estate tax exemptions but creates a clear division that provides for your spouse while guaranteeing your children’s inheritance.

These trust structures solve the central challenge of blended family estate planning: caring for your current spouse while ensuring your assets ultimately reach your children.

ILIT & Life Insurance: Instant Equalizer

Life insurance offers perhaps the most neat solution for blended families—creating new wealth rather than dividing existing assets. When held in an Irrevocable Life Insurance Trust (ILIT), it becomes even more powerful.

Think of life insurance as creating an immediate inheritance fund for children from previous marriages, while allowing other assets to pass to your spouse. This approach reduces potential resentment and conflict, as each beneficiary receives meaningful support without feeling in competition with others.

The ILIT keeps insurance proceeds outside your taxable estate and provides immediate liquidity for expenses and taxes. Many families fund their ILIT through annual gift tax exclusions ($18,000 per beneficiary in 2024), making it an accessible strategy for creating inheritance equality.

Beneficiary Designations & Pay-on-Death Accounts

Some of your most valuable assets—retirement accounts, life insurance, and financial accounts—bypass your will or trust entirely, making beneficiary designations critically important.

Your 401(k) and employer retirement plans legally must go to your current spouse unless they sign a waiver—a fact that surprises many people in blended families. IRAs offer more flexibility in naming beneficiaries, but most non-spouse beneficiaries now face the SECURE Act’s 10-year distribution rule, accelerating tax consequences.

Pay-on-Death (POD) and Transfer-on-Death (TOD) designations on bank and investment accounts allow immediate transfer without probate—convenient, but potentially problematic if they don’t align with your overall plan.

Because these designations override your will and trust, they require special attention in blended family estate planning. We recommend reviewing all beneficiary forms after every major life event (marriage, divorce, births, deaths), at least annually, and whenever tax laws change. An outdated beneficiary form can undo years of careful planning in an instant.

Balancing Fairness & Avoiding Family Fights

Perhaps the greatest challenge in blended family estate planning is maintaining family harmony while ensuring everyone’s needs are met. This balancing act requires thoughtful consideration of both legal and emotional factors.

Open Communication Strategies

When I meet with blended families, I often remind them that the best legal documents in the world can’t replace honest conversation. Open communication forms the foundation of successful planning and helps prevent painful misunderstandings later.

Family meetings can be incredibly powerful tools. You don’t need to share specific dollar amounts, but gathering adult family members to discuss your general intentions creates understanding. I’ve seen these conversations transform potential conflicts into opportunities for family bonding.

Consider supplementing your legal documents with a heartfelt letter of intent. These personal messages explain the thinking behind your estate plan in your own words. They’re not legally binding, but they help heirs understand your values and motivations, often answering the crucial “why” questions that legal documents don’t address.

For additional protection, we often recommend no-contest clauses. These provisions discourage challenges to your will or trust by potentially disinheriting anyone who contests the document. While not perfect, they add an extra layer of security for your wishes.

One of my favorite success stories involved a couple who created a simple flowchart showing how assets would transfer after each death. They shared this visual with their adult children, which sparked meaningful conversations about their legacy. The clarity this provided prevented years of potential misunderstandings.

Professional or Independent Trustees

Choosing the right trustee is one of the most consequential decisions in blended family estate planning. Think of your trustee as the person who will speak for you when you no longer can.

Family member trustees bring personal knowledge and often serve without compensation. However, they may face accusations of favoritism or find themselves caught in difficult family dynamics. I’ve seen many well-meaning family trustees struggle with the emotional burden of these roles.

Professional trustees offer neutrality and expertise that can be invaluable for blended families. Banks, trust companies, and law firms like ours understand the legal complexities and can make impartial decisions without emotional messs. Yes, there are fees involved, but many families find the peace of mind well worth the cost.

Some families find the perfect balance with co-trustees, pairing a family member with a professional. This approach combines personal knowledge with professional oversight. The family member provides the “heart” while the professional brings the “head” to decision-making.

Choosing a trustee isn’t just about who’s most qualified—it’s about who can best preserve family relationships through potentially difficult transitions.

Using Life Insurance to Level the Field

Life insurance is perhaps the most powerful tool in our blended family estate planning toolkit. It creates an immediate, separate inheritance that can solve many complex family situations with neat simplicity.

By creating distinct asset pools for different beneficiaries, life insurance minimizes the potential for conflict. Your current spouse can receive your retirement accounts and home, while children from a previous marriage receive equivalent value through insurance proceeds. This approach allows everyone to feel fairly treated without forcing them to share assets or make decisions together.

Life insurance also provides immediate liquidity when families need it most. While estates can take months or years to settle, insurance proceeds typically arrive within weeks, providing crucial financial support during difficult transitions.

For families with businesses or significant estate tax concerns, insurance can provide funds for buyouts or tax payments, preserving other assets for heirs. This strategic approach keeps family businesses intact while ensuring equitable treatment for all children.

The beauty of insurance in blended family situations is its clarity—it creates clean lines of inheritance that reduce friction points. When each branch of the family has their own resources, they’re free to focus on healing rather than fighting over assets.

At Daughtry, Woodard, Lawrence & Starling, we’ve guided hundreds of North Carolina families through these sensitive conversations. We understand that successful blended family estate planning isn’t just about legal documents—it’s about creating a framework for continued family harmony that honors all the relationships you value.

Special Considerations: Minors, Special-Needs, and Taxes

Blended family estate planning takes on additional layers of complexity when minor children, beneficiaries with special needs, or significant tax considerations enter the picture.

Planning for Minor Children in Blended Family Estate Planning

When your blended family includes young children, thoughtful planning becomes even more crucial. One of the most important decisions you’ll make is naming guardians for minor children if both biological parents pass away. This designation carries extra weight in blended families, as step-parents don’t automatically receive custody without proper documentation.

Beyond guardianship, you’ll need to consider how assets will be managed for children until they reach adulthood. UTMA/UGMA accounts offer one option, providing a straightforward way to set aside funds for minors. However, these accounts come with limitations—namely that children gain full control of the assets between ages 18-21 (depending on your state), which may not align with your wishes.

For greater control and protection, children’s trusts offer a more flexible alternative. These specialized trusts can fund education, maintenance, and ongoing support while protecting assets until children reach the ages you specify—perhaps receiving portions at 25, 30, and 35 rather than all at once.

The selection of trustees becomes particularly important here. Ideally, you’ll choose someone who will advocate strongly for your children’s interests, especially if this person differs from the guardian. At Daughtry, Woodard, Lawrence & Starling, we help families steer these guardianship provisions with sensitivity to the unique dynamics of blended families.

Special-Needs Beneficiaries & Government Benefits

For blended families caring for members with special needs, estate planning requires an additional level of expertise to balance government benefits with family support.

Special Needs Trusts (SNTs) form the cornerstone of this planning. These specialized vehicles allow you to improve a disabled beneficiary’s quality of life without jeopardizing essential government benefits like SSI and Medicaid. Third-party SNTs—created and funded by someone other than the beneficiary themselves—offer the most flexibility and protection in a blended family situation.

Many families complement SNTs with ABLE accounts, which provide tax-advantaged savings opportunities for disabled beneficiaries. These accounts work alongside trusts to create a comprehensive support system.

The trustee you select for a special needs trust should have familiarity with both government benefit regulations and the beneficiary’s specific needs. This combination of knowledge becomes even more vital in blended families where communication channels may be more complex.

As we often explain to parents of children with special needs, proper planning doesn’t just preserve benefits—it can dramatically improve quality of life for your loved one while providing peace of mind for everyone involved.

Tax Traps & Opportunities

The intersection of taxes and blended family estate planning creates both challenges and opportunities that deserve careful attention.

The unlimited marital deduction offers a powerful tax advantage, allowing you to transfer unlimited assets to a U.S. citizen spouse free of estate and gift taxes. This effectively defers any estate tax until the second spouse’s death—a valuable tool for blended families looking to maximize what remains for the next generation.

Portability represents another opportunity, allowing a surviving spouse to use their deceased spouse’s unused estate tax exemption. However, this benefit isn’t automatic—it requires proper planning and timely filing of estate tax returns, even when no tax is due.

Lifetime gifting strategies can help reduce your taxable estate while benefiting heirs during your lifetime. Annual exclusion gifts (currently $18,000 per recipient in 2024) allow you to transfer wealth gradually without triggering gift taxes.

The stepped-up basis rule provides a significant tax advantage for inherited assets, as beneficiaries receive property with a tax basis equal to its fair market value at your death. This potentially eliminates capital gains tax on appreciation that occurred during your lifetime—a consideration worth factoring into your asset distribution strategy.

For families with substantial assets, the generation-skipping transfer tax may come into play when assets pass to grandchildren or more remote descendants. Without careful planning, this additional tax can take a significant bite out of your legacy.

The tax landscape for blended families certainly presents challenges, but with thoughtful planning, you can minimize tax burdens while maximizing what passes to your loved ones. Proper asset titling and long-term care considerations should also factor into your comprehensive plan.

At Daughtry, Woodard, Lawrence & Starling, we guide families through these complex considerations with clarity and compassion, helping you create a plan that protects everyone you love while preserving family harmony for generations to come.

Conclusion

Creating a plan that works for everyone in your blended family isn’t just about legal documents—it’s about protecting relationships and ensuring peace of mind for the people you love most.

Throughout this guide, we’ve explored how blended family estate planning differs from traditional approaches. We’ve seen how specialized trusts can protect both current spouses and children from previous relationships. We’ve discussed the importance of clear communication and regular updates as family dynamics evolve.

The truth is, without thoughtful planning, even the most harmonious blended families can face unexpected challenges when a loved one passes away. But it doesn’t have to be that way.

At Daughtry, Woodard, Lawrence & Starling, we’ve guided hundreds of North Carolina families through these complex waters. We’ve seen how proper planning transforms uncertainty into confidence and potential conflict into family harmony.

Your estate plan should grow and change as your family does. Life events like births, marriages, divorces, and changes in relationships should trigger a review of your plan. Tax laws change, too—what worked perfectly five years ago might need adjustments today.

The most successful blended families approach estate planning as an ongoing conversation rather than a one-time task. They recognize that open communication about intentions (even when difficult) prevents painful surprises later.

Your family deserves a plan as unique as your story. Whether you’re just starting to think about these issues or need to update an existing plan, our experienced team at Daughtry, Woodard, Lawrence & Starling is here to help. Our board-certified specialists understand the nuances of blended family estate planning and can guide you through creating a solution that works for everyone you love.

We invite you to learn more about our estate planning services and how our compassionate, bilingual staff can support your family’s journey. Serving families throughout Smithfield, Clinton, and Sampson County, we’re committed to providing the personalized guidance your blended family needs to thrive for generations to come.

Don’t leave your family’s future to chance. With thoughtful planning today, you can create a legacy of care that honors all the relationships that make your blended family special.

Frequently Asked Questions

Do stepchildren inherit automatically?

One of the most common questions I hear in my office comes with a look of genuine concern: “Will my stepchildren be taken care of when I’m gone?”

The answer is straightforward but often surprising to many families. Under North Carolina law (and most state laws), stepchildren have no automatic inheritance rights unless they’ve been legally adopted. Without specific provisions naming them in your estate plan, your stepchildren will receive nothing when you pass away—regardless of how close your relationship might be.

This legal reality is why being explicit about including stepchildren in your will, trust, or beneficiary designations is absolutely essential. You have complete flexibility in how you approach this—you might choose to treat stepchildren identically to biological children, provide different inheritance amounts, or create special conditions custom to your family’s unique dynamics.

Many of our clients at Daughtry, Woodard, Lawrence & Starling find that trusts offer the perfect solution for providing for stepchildren while maintaining thoughtful control over how and when assets are distributed. Others prefer using life insurance policies that name stepchildren as beneficiaries, creating separate inheritance streams that don’t compete with provisions for biological children.

Should spouses create joint or separate estate plans?

When Melissa and Robert came to our office, they were convinced a joint estate plan was the simplest approach—until we discussed their blended family’s specific needs.

For most blended families, separate estate plans actually provide better protection for each spouse’s unique family interests. While joint plans work beautifully for first marriages with only shared children, blended families typically benefit from individual wills and trusts that address each spouse’s specific wishes for their biological children and stepchildren.

That said, coordination between these separate plans is absolutely essential. We often help couples create complementary estate plans that work together harmoniously to achieve shared goals while protecting each spouse’s individual priorities. Think of it as two instruments playing different parts of the same beautiful song.

Some couples also benefit tremendously from prenuptial or postnuptial agreements that clearly distinguish separate property from marital property. These agreements can form a solid foundation for estate plans that fairly balance competing interests and help prevent future conflicts among family members.

How often should a blended family update its estate plan?

“Life changes quickly in blended families,” as one of my clients wisely noted. That’s why blended family estate planning requires more frequent reviews than traditional family plans—ideally every 2-3 years rather than the standard 3-5 years.

Updates become particularly important after life’s inevitable transitions:

Marriage or divorce, birth or adoption of children, death of a beneficiary, significant changes in asset values, relocation to another state, tax law changes, and shifts in family relationships all signal it’s time for a review.

I remember one client who hadn’t updated her plan in seven years—during which time her relationship with her stepson had blossomed from awkward to deeply loving. Her outdated plan left him nothing, completely misrepresenting her current wishes. Regular reviews ensure your plan continues to reflect your current relationships and family circumstances.

As relationships evolve in blended families—and they almost always do—your estate plan should adapt accordingly. The document you create today should never be set in stone, but rather grow and change as your family does.