Why Estate Planning for Seniors Is More Critical Than Ever

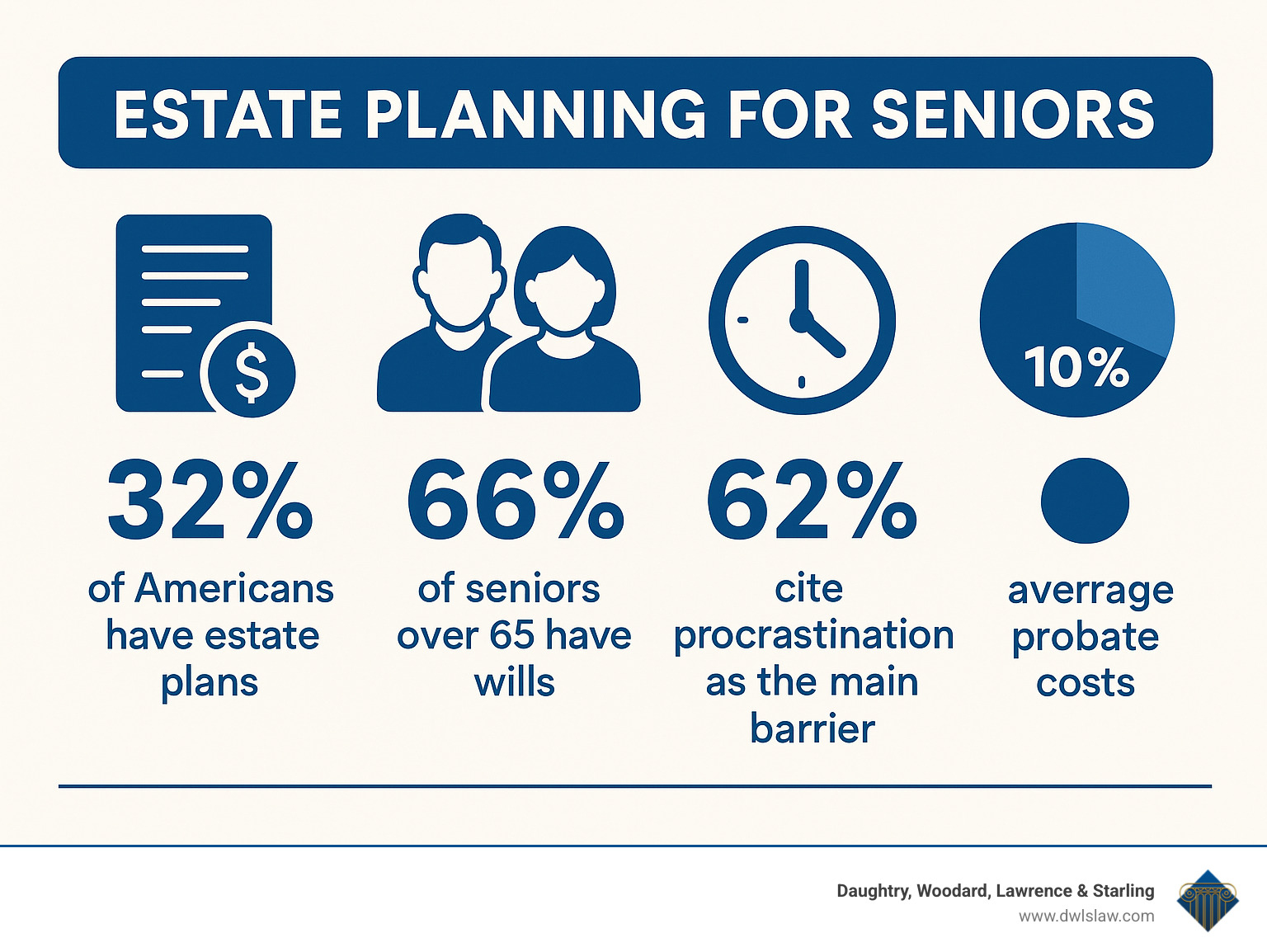

Estate planning for seniors protects your legacy, ensures your wishes are honored, and provides peace of mind for you and your loved ones. Yet nearly half of Americans over 55 don’t have a will, and only 32% have created a comprehensive estate plan.

Essential estate planning components for seniors include:

• Last Will & Testament – Names beneficiaries and executor

• Revocable Living Trust – Avoids probate and provides privacy

• Financial Power of Attorney – Manages finances if incapacitated

• Healthcare Directive – Guides medical decisions

• Beneficiary Designations – Ensures accounts transfer properly

The stakes get higher as we age. Without proper planning, your family faces expensive probate court proceedings that can consume up to 10% of your estate’s value. More importantly, they may struggle to make critical healthcare and financial decisions if you become incapacitated.

The good news? Creating an estate plan doesn’t require vast wealth or complex legal maneuvers. Whether you own a modest home or significant assets, proper planning ensures your wishes are respected and your loved ones are protected.

This guide walks you through everything seniors need to know about estate planning – from essential documents to tax strategies to family communication. You’ll learn practical steps to protect your assets, plan for potential incapacity, and create a lasting legacy.

I’m Kelly K. Daughtry, and I’ve spent over five decades helping North Carolina families steer estate planning challenges with compassion and expertise. My experience with estate planning for seniors has shown me that the right plan, created at the right time, transforms anxiety into confidence for both seniors and their families.

Estate Planning for Seniors: Why It Matters

If you’re among the 50 million Americans aged 65 or older, you’re part of a rapidly growing demographic that faces unique legal and financial challenges. That’s roughly one in every seven Americans—and the numbers keep climbing.

Here’s what might surprise you: despite the growing need, most seniors haven’t taken the essential steps to protect themselves and their families. The consequences of this gap can be devastating.

Without a proper estate plan, your family enters dangerous territory. Probate court proceedings stretch on for months, sometimes over a year, while legal fees and court costs chip away at the assets you worked a lifetime to build. During this painful process, your loved ones may find themselves unable to access the funds they desperately need for daily expenses or even your final arrangements.

The emotional weight on family members becomes crushing when they’re left guessing about your wishes. We’ve watched adult children battle in court over who should make decisions for an incapacitated parent. We’ve seen siblings torn apart arguing about medical care. We’ve comforted spouses who couldn’t access their own joint accounts when they needed them most.

The financial reality makes planning even more urgent. Scientific research on long-term care costs paints a sobering picture of what families face. Long-term care expenses continue skyrocketing, with nursing home costs often exceeding $8,000 to $12,000 per month in many areas. At that rate, a lifetime of careful saving can vanish in just a few short years.

But here’s the good news: estate planning for seniors transforms this anxiety into genuine peace of mind. It’s not just about protecting money—though that matters. It’s about preserving your voice and ensuring your wishes guide every decision, even when you can’t speak for yourself.

What Is Estate Planning for Seniors?

Think of estate planning for seniors as your comprehensive roadmap for both living well and leaving well. It goes far beyond the simple question of “who gets what” after you’re gone.

Your estate plan addresses the real challenges of aging—what happens if you can’t make decisions for yourself, how to handle healthcare choices, planning for potential long-term care needs, and protecting your assets from unnecessary depletion. This differs significantly from basic estate planning because it specifically tackles age-related concerns like Medicare planning, Social Security optimization, and protection against elder financial abuse.

Many people confuse elder law with estate planning, but they serve different purposes. Elder law focuses on your rights and needs while you’re living—things like qualifying for Medicaid benefits, preventing abuse, and ensuring you receive appropriate care. Estate planning centers on who makes decisions and how your assets are distributed, both during any period of incapacity and after your death.

The ultimate goal is preserving your autonomy. When your estate plan is properly crafted, you maintain control over your affairs even as your circumstances change. Your preferences become the guiding light for every decision that affects your life and legacy.

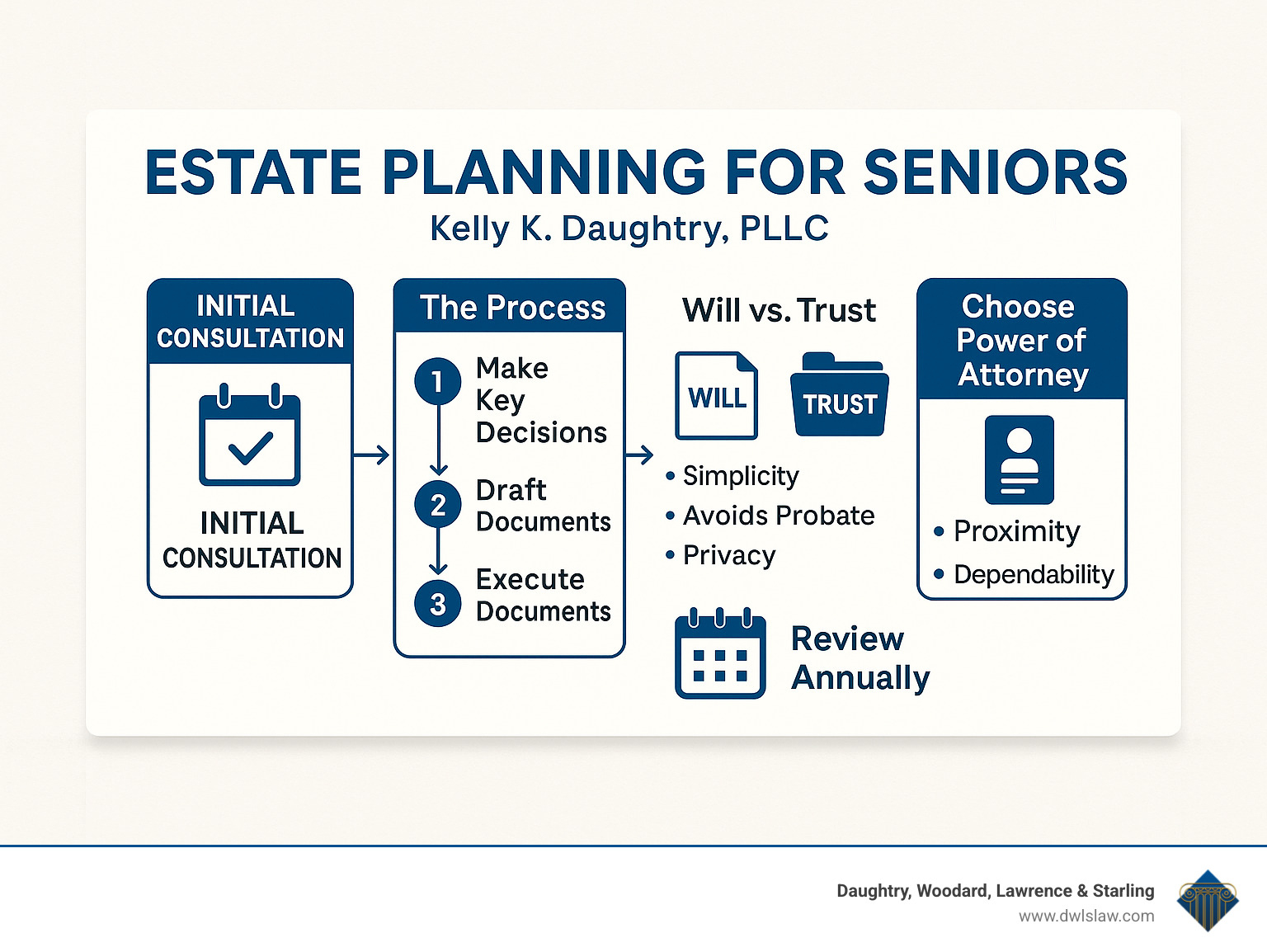

When Should Seniors Start & How Often to Review?

The honest answer about timing? The best time to start your estate planning was yesterday. The second-best time is today.

That said, certain life events should trigger immediate action. Reaching age 65 or retirement marks a natural transition point when estate planning becomes more urgent. A diagnosis of any serious medical condition demands immediate attention to your planning. Changes in your family structure—whether through marriage, divorce, or the death of a spouse—require updates to your documents.

Significant changes in your assets or financial situation also signal time for a review, as does moving to a different state, since laws vary significantly across state lines.

We strongly recommend reviewing your estate plan every three to five years, or whenever major life changes occur. More info about plan reviews helps explain why keeping your documents current is so critical.

Here’s a mistake we see repeatedly: seniors think they’ve “finished” their estate planning after signing the initial documents. In reality, estate planning is an ongoing conversation between you and your plan. Your needs evolve, your family circumstances change, and laws get updated. Your estate plan should grow and adapt right alongside your life.

Core Estate-Planning Documents & Tools

Think of estate planning for seniors like assembling a toolkit—each document serves a specific purpose, and together they create a comprehensive safety net for you and your family. The right combination of tools ensures your wishes are honored and your loved ones are protected, no matter what life brings.

At the heart of every senior’s estate plan, you’ll find several essential documents working together. Your last will and testament provides the foundation, while trusts offer privacy and probate avoidance. Powers of attorney handle your affairs during incapacity, and beneficiary designations ensure accounts transfer smoothly. Additional tools like pour-over wills and life estate deeds fill in any gaps.

The beauty of proper estate planning lies in how these documents complement each other. Your will might distribute personal belongings and name guardians, while your trust handles major assets like your home and investments. Your power of attorney manages day-to-day finances if you become ill, and your healthcare directive guides medical decisions.

Many seniors wonder whether they need both a will and a trust. The answer often depends on your specific situation, but most comprehensive plans include both. Here’s how they compare:

| Feature | Will | Revocable Living Trust |

|---|---|---|

| Probate Required | Yes | No |

| Privacy | Public record | Private |

| Time to Distribute | 6+ months | Days to weeks |

| Cost to Create | Lower | Higher |

| Incapacity Planning | No | Yes |

| Asset Protection | Limited | Moderate |

Understanding these differences helps you make informed decisions about which combination best serves your family’s needs and your personal goals.

Last Will & Testament – The Foundation

Your will tells the world exactly how you want your affairs handled after you’re gone. For seniors, this document becomes even more important because it addresses concerns that younger people might not yet face—like caring for an aging spouse or distributing a lifetime’s worth of accumulated belongings.

The executor you choose carries enormous responsibility. This person will gather your assets, pay your debts, file necessary tax returns, and distribute your property according to your instructions. Many seniors choose their most organized and trustworthy adult child, though a close friend or professional can also serve effectively. The key is selecting someone who lives nearby, understands your wishes, and can handle both emotional and financial pressures.

If you’re still caring for minor children or grandchildren, your will lets you name guardians who share your values and parenting philosophy. Without this crucial designation, courts make these life-changing decisions without knowing your preferences or the children’s needs.

Your will also handles the personal touches that matter most to families. Maybe you want your grandmother’s wedding ring to go to a specific granddaughter, or you’d like your fishing gear donated to a local youth program. These personal bequests often mean more to families than the financial aspects of inheritance.

Even if you create a trust, you’ll still need what’s called a pour-over will. This safety net catches any assets you forgot to transfer into your trust during your lifetime. More info about wills can help you understand all the components that make a will truly effective.

Yes, wills must go through probate court, which takes time and costs money. But they remain the foundation of most estate plans because they handle responsibilities that other documents simply can’t address.

Trusts That Help Seniors

Trusts might sound complicated, but they’re really just legal containers that hold your assets and distribute them according to your instructions. For seniors, trusts offer three major advantages: avoiding probate, maintaining privacy, and providing management during incapacity.

Revocable living trusts are the most popular choice for seniors because they offer flexibility with protection. You remain in complete control as the trustee, managing your assets exactly as you always have. If you become incapacitated, your chosen successor trustee steps in seamlessly—no court involvement required. When you pass away, your assets transfer directly to beneficiaries without the delays and expenses of probate court.

Irrevocable trusts require giving up control but offer stronger protection. For seniors worried about nursing home costs, Medicaid asset protection trusts can shelter assets from long-term care expenses while still providing you with income. These trusts must be established well before you need care due to Medicaid’s five-year look-back period.

Special needs trusts solve a common dilemma for seniors who want to provide for disabled family members without jeopardizing their government benefits. These trusts supplement—rather than replace—benefits like Medicaid and Supplemental Security Income.

Spendthrift trusts protect inheritances from beneficiaries who might struggle with money management, addiction, or creditor problems. Instead of receiving a lump sum, beneficiaries receive regular distributions that can’t be seized by creditors or spent impulsively.

The secret to successful trust planning is proper funding—actually transferring assets into the trust’s name. A trust without assets is like a bank account without money—it exists but doesn’t accomplish your goals.

Powers of Attorney & Health Care Directives

These documents often prove more immediately valuable than wills or trusts because they protect you while you’re still alive. Without them, your family faces expensive and time-consuming court proceedings just to help you during a medical crisis.

A financial power of attorney authorizes someone you trust to handle your money matters if you become incapacitated. Your agent can pay bills, manage investments, handle insurance claims, and make necessary financial decisions. Choose someone who lives nearby, understands your financial situation, and shares your values about money management.

Healthcare powers of attorney (also called healthcare proxies) designate someone to make medical decisions when you can’t speak for yourself. This person should understand your feelings about quality of life, medical intervention, and end-of-life care. Many seniors choose different people for financial and healthcare decisions based on each person’s strengths and availability.

Living wills provide specific instructions about medical treatments you do or don’t want in various scenarios. You might address questions about life support, feeding tubes, resuscitation efforts, pain management, and organ donation. The more specific your instructions, the easier you make things for both your family and your medical team.

Don’t forget HIPAA authorization, which allows your designated agents to access medical records and communicate with healthcare providers. Scientific research on advance care planning shows that people who complete advance directives receive care that better matches their personal preferences and values.

Without these documents, your family may need court-appointed guardianship or conservatorship to help you—expensive processes that can take months and may result in decisions you wouldn’t approve. The right documents ensure your trusted loved ones can act immediately when you need help most.

Protecting Assets, Minimizing Taxes & Avoiding Probate

For many seniors, protecting hard-earned assets from unexpected expenses ranks as their top concern. After decades of saving and building wealth, the thought of losing everything to nursing home costs or lengthy probate proceedings keeps many people awake at night.

The reality is sobering: long-term care costs can easily exceed $100,000 per year in many areas. Without proper planning, a lifetime of savings can disappear in just a few years. But here’s the encouraging news—smart planning strategies can help protect your assets while ensuring you receive the care you need.

Long-term care insurance offers one solution, covering nursing home expenses, in-home care, and assisted living costs that Medicare won’t touch. Unfortunately, many seniors find these policies have become prohibitively expensive or find they no longer qualify due to health changes. That’s where other planning strategies become essential.

Medicaid planning requires understanding the five-year look-back period that scrutinizes any asset transfers before applying for benefits. Make a gift to your grandchildren or transfer property to your children within five years of needing Medicaid, and you might face penalties that delay your eligibility. However, certain transfers—like those to a disabled child or into properly structured trusts—won’t trigger these penalties.

Strategic gifting allows you to reduce your taxable estate while helping family members when they might need it most. The annual gift tax exclusion lets you give a specific amount to each person without triggering taxes or eating into your lifetime exemption. It’s like having your cake and eating it too—you get to see your family benefit from your generosity while reducing potential estate taxes.

Joint ownership and transfer-on-death (TOD) or payable-on-death (POD) designations provide straightforward ways to pass assets without probate court involvement. Simply add your adult child’s name to your bank account or designate them as the TOD beneficiary on your investment account, and those assets transfer automatically upon your death.

But beware—these simple solutions come with hidden risks. Joint ownership means your co-owner can access and potentially drain your accounts while you’re alive. Their creditors might also target your assets if they face financial troubles.

Understanding current estate and inheritance tax thresholds helps you make informed decisions. While federal estate taxes only affect the wealthiest Americans, some states impose their own taxes at much lower levels. More info about long-term care options can help you explore the full range of strategies available for your situation.

Probate-Avoidance Techniques for Seniors

Nobody wants their family dealing with probate court while they’re grieving. The process can drag on for months, consume thousands of dollars in fees, and turn your private family matters into public records that anyone can access.

Revocable trust funding represents the gold standard for probate avoidance. This involves changing the ownership of your assets from your individual name to your trust’s name. Your home, bank accounts, investment portfolios, and even your car can be retitled in the trust’s name. When you pass away, your successor trustee can distribute these assets according to your wishes without any court involvement.

The beauty of this approach lies in its simplicity for your family. Instead of waiting months for probate approval, your trustee can typically begin distributing assets within days or weeks of your death. Your family gets the resources they need when they need them most.

Beneficiary designations offer another powerful probate-avoidance tool that many seniors overlook. These forms on your retirement accounts, life insurance policies, and bank accounts override whatever your will says and transfer assets directly to your named beneficiaries. Just remember to keep these forms current—we’ve seen too many cases where outdated designations sent assets to ex-spouses or people who died years earlier.

Life estate deeds provide a specialized solution for your home. You can transfer ownership to your children while keeping the right to live there for the rest of your life. Upon your death, they automatically become full owners without any probate proceedings. However, this strategy limits your flexibility and may create unexpected tax consequences.

Small estate affidavits offer simplified procedures for modest estates that don’t justify the expense of full probate proceedings. Each state sets different thresholds and requirements, but these expedited processes can save your family significant time and money when applicable.

Estate & Income Tax Playbook

While most seniors won’t face federal estate taxes thanks to generous exemption amounts, smart tax planning can still put more money in your beneficiaries’ pockets and less in Uncle Sam’s.

Annual gifting strategies let you shrink your taxable estate while watching your family benefit from your generosity. Beyond the standard annual exclusion amounts, you can pay unlimited amounts directly to educational institutions for someone’s tuition or to medical providers for their healthcare expenses. These payments don’t count against your annual limits, making them powerful tools for grandparents wanting to help with college costs or medical bills.

Portability elections offer married couples a valuable opportunity to effectively double their estate tax protection. When your spouse dies, you can claim their unused federal estate tax exemption in addition to your own. However, this benefit requires filing a federal estate tax return within nine months of death, even if no taxes are owed—a requirement many families miss.

Charitable giving provides the satisfying combination of supporting causes you care about while reducing your tax burden. Beyond simple cash donations, charitable remainder trusts can provide you with income for life while ultimately benefiting your chosen charities. It’s a win-win strategy that supports your values while providing tax benefits.

Roth IRA conversions represent one of the most powerful tax strategies available to seniors. By paying taxes now on traditional IRA funds and converting them to Roth IRAs, you create completely tax-free inheritance assets for your beneficiaries. This strategy works particularly well when your income temporarily drops or when you expect tax rates to increase in the future.

The key to successful estate planning for seniors lies in understanding how these various strategies work together to protect your assets, minimize taxes, and ensure your family receives their inheritance efficiently and privately.

Incapacity, Emergencies & End-of-Life Planning

Nobody likes to think about losing their independence or facing serious health challenges. But for seniors, planning for these possibilities isn’t just wise—it’s essential. The sobering reality is that one in three older adults dies with Alzheimer’s disease or another form of dementia, making estate planning for seniors even more critical.

The goal isn’t to dwell on worst-case scenarios, but to create a safety net that protects your autonomy and guides your family when you can’t speak for yourself. When you plan ahead, you maintain control over your care and give your loved ones clear direction during what will already be a stressful time.

Durable powers of attorney form the backbone of incapacity planning because they continue working even after you become unable to make decisions. Unlike regular powers of attorney that become useless the moment you need them most, durable versions keep your chosen agents in charge throughout any period of incapacity.

Your living will should paint a clear picture of your preferences for different medical scenarios. Think about whether you want aggressive treatment if you’re terminally ill, or if you’d prefer comfort-focused care that prioritizes dignity and pain relief over extending life at any cost.

Do Not Resuscitate (DNR) orders and Physician Orders for Life-Sustaining Treatment (POLST) forms give immediate guidance to paramedics and emergency room staff. If you have strong feelings about resuscitation or life support, make sure these documents are easily found and clearly displayed where you live.

Organ donation decisions deserve thoughtful consideration and family discussion. Whether you choose to donate or not, make your wishes known through your advance directives and talk with your family so they understand and can support your choice during an emotional time.

Estate Planning for Seniors in Medical Crisis

When health emergencies strike without warning, having the right documents in place can mean the difference between your wishes being honored and your family scrambling to figure out what you would have wanted.

Healthcare proxy activation needs clear triggers defined in your documents. Some families prefer that the healthcare power of attorney kicks in immediately, while others want it activated only when a doctor determines you’re incapacitated. Consider your comfort level with sharing decision-making and your family’s ability to work together under pressure.

Hospital staff work with these situations daily, but they need to see original or certified copies of your healthcare directives and powers of attorney. A photo on your phone might help in a pinch, but official documents carry the legal weight needed to ensure your instructions are followed.

Portable directives become especially important if you travel frequently or spend time in multiple states. While most states recognize properly executed documents from other states, some have specific forms or requirements that could create delays when you need immediate care.

Safeguarding Digital & Physical Records

Today’s seniors often have one foot in the digital world and one in the traditional paper world, which means your estate planning must protect both types of important information.

Password managers help organize the growing collection of online accounts that control everything from banking to social media to digital photo collections. Choose a reputable service and make sure your trusted agents know how to access the master password or recovery information when they need it.

Fire-safe boxes or bank safe deposit boxes protect your original documents from disasters and theft, but they’re only helpful if the right people can get to them quickly. Make sure your agents know where these boxes are located and have the keys or access codes they’ll need.

Cloud vaults and digital storage services create secure backup copies of important documents while allowing authorized access from anywhere with an internet connection. This can be a lifesaver when your agent needs to access your healthcare directive from a hospital across the country.

More info about choosing a health care agent can help you think through who’s best equipped to handle these responsibilities and how to give them the tools they need to succeed.

Consider creating a comprehensive inventory that includes account numbers, contact information for your financial advisors and attorneys, locations of important documents, and step-by-step instructions for accessing digital assets. Think of it as a roadmap that guides your family through the practical details when they’re dealing with the emotional stress of your health crisis.

Family Dynamics, Special Situations & Updating Your Plan

Estate planning for seniors often involves complex family dynamics that require careful consideration and sensitive handling. Blended families, second marriages, and stepchildren create unique challenges that demand thoughtful planning approaches.

In second marriages, spouses must balance providing for each other while ensuring children from previous relationships receive intended inheritances. Prenuptial agreements, qualified terminable interest property (QTIP) trusts, and life insurance can help address competing interests.

Special needs beneficiaries require specialized planning to preserve their eligibility for government benefits while providing supplemental support. Special needs trusts allow you to leave assets that improve their quality of life without disqualifying them from Medicaid, Supplemental Security Income, or other crucial programs.

Pet trusts provide legal mechanisms for ensuring beloved animals receive proper care after your death. While some might consider this frivolous, pets often provide crucial emotional support for seniors, making their continued care a legitimate estate planning concern.

Creditor protection becomes important when beneficiaries face financial difficulties, divorce proceedings, or professional liability issues. Spendthrift trusts and discretionary distribution provisions can protect inheritances from creditors while still providing support for beneficiaries’ needs.

Communication & Conflict-Prevention

Open communication prevents many estate planning conflicts that tear families apart after a senior’s death. Family meetings provide opportunities to explain your decisions, address concerns, and ensure everyone understands their roles and responsibilities.

Letters of instruction supplement legal documents by explaining your reasoning behind specific decisions, sharing family history, and providing guidance for situations not covered in formal documents. These personal messages often prove more valuable to families than the legal documents themselves.

When family conflicts seem inevitable, consider involving a professional mediator in planning discussions. Neutral third parties can help facilitate difficult conversations and find solutions that respect everyone’s concerns while honoring your wishes.

When Life Changes—Keep Your Estate Planning for Seniors Current

Estate plans require regular updates to remain effective and reflect your current wishes. Major life events that should trigger plan reviews include births, deaths, marriages, divorces, significant changes in health or finances, and changes in applicable laws.

Birth of grandchildren might prompt you to add new beneficiaries or create education trusts. Death of named agents requires selecting new individuals for powers of attorney and executor roles. Marriage or divorce typically necessitates comprehensive plan revisions.

Changes in tax laws can affect the effectiveness of your planning strategies. The federal estate tax exemption, for example, is scheduled to decrease significantly in 2026 unless Congress acts to extend current levels.

More info about updating a will provides detailed guidance on recognizing when changes are needed and ensuring updates are properly executed.

Frequently Asked Questions about Estate Planning for Seniors

After helping North Carolina families with estate planning for seniors for decades, I’ve heard countless questions from concerned families. Here are the most common concerns and straightforward answers that might help ease your worries.

What happens if I die without a will?

Dying without a will—what lawyers call “intestacy”—means North Carolina state law makes all the important decisions about your estate instead of you. Your assets get distributed according to a rigid formula that might not reflect what you actually wanted.

In North Carolina, if you’re married with children, your spouse typically receives the first $60,000 plus half of the remaining estate, while your children split the rest. If you’re unmarried, your children inherit everything equally. No children? Your parents or siblings might inherit assets you intended for someone else entirely.

The court appoints an administrator to handle your estate, and this person might not be who you would have chosen. Maybe you trusted your responsible daughter Sarah to handle things, but the court appoints your well-meaning but disorganized son instead. The process typically takes longer and costs more than when you have a proper will guiding the way.

Your family also misses out on your personal guidance about treasured belongings, special instructions, and the reasoning behind your decisions. That antique rocking chair with sentimental value might end up with the wrong grandchild simply because no one knew your wishes.

Is a revocable living trust better than a will for seniors?

This question doesn’t have a one-size-fits-all answer, but revocable living trusts do offer compelling advantages for many seniors. The biggest benefits include avoiding probate court entirely, keeping your affairs private, and providing seamless management if you become incapacitated.

When your assets are in a properly funded trust, your successor trustee can distribute them to beneficiaries within days or weeks rather than the six months or more that probate typically requires. Your family’s financial information stays private instead of becoming public court records that anyone can access.

The incapacity planning benefits often prove most valuable. If you develop dementia or suffer a stroke, your successor trustee can immediately step in to manage your finances without requiring court intervention. With just a will, your family might need expensive guardianship proceedings to gain authority over your affairs.

However, trusts cost more to create upfront and require ongoing attention to ensure all your assets are properly transferred into the trust’s name. Many seniors find the best approach combines both: a revocable living trust for major assets plus a “pour-over” will to catch anything you forgot to transfer.

The right choice depends on your specific situation, family dynamics, and comfort level with ongoing trust maintenance. Most seniors with homes, significant retirement accounts, or concerns about incapacity benefit from trust-based planning.

How can I protect my home from nursing-home costs?

Protecting your home from long-term care costs requires advance planning, but several effective strategies can help preserve this important asset for your family while ensuring you receive necessary care.

Medicaid asset protection trusts offer one of the strongest protection methods. You can transfer your home into an irrevocable trust while retaining the right to live there for life. After the five-year Medicaid look-back period expires, the home is protected from nursing home costs. The downside? You give up ownership and control, so this strategy requires careful consideration.

Life estate deeds provide another option by transferring ownership to family members while preserving your lifetime right to live in the home. Upon your death, ownership passes automatically to your chosen recipients without probate. This approach offers some protection but less flexibility than trust-based planning.

Long-term care insurance represents a different approach entirely—covering nursing home costs directly so you don’t need to spend down your assets first. While policies can be expensive, they provide peace of mind and asset protection for families who can afford the premiums.

Strategic gifting and family partnerships might work for some situations, but these approaches require careful timing and professional guidance to avoid Medicaid penalties.

The key insight? All effective home protection strategies require advance implementation. Waiting until you need nursing home care severely limits your options. Most protective techniques need several years to become fully effective, making early planning essential for success.

Conclusion

Estate planning for seniors isn’t just about paperwork—it’s about changing worry into confidence and uncertainty into clear direction. When you take the time to create a comprehensive plan, you’re giving yourself and your family an incredible gift: the peace of mind that comes from knowing everything is handled exactly as you want it.

Think of estate planning as an ongoing conversation with your future self and your loved ones. It’s not something you do once and forget about. Life keeps changing, and your plan should change with it. New grandchildren arrive, health situations evolve, and laws shift. The families who fare best are those who view their estate plan as a living document that grows and adapts over time.

We’ve seen countless families who thought they could put off these important decisions. The truth is, there’s never a “perfect” time to start planning, but there’s always a right time—and that time is now. Whether you’re 55 or 85, whether you own a modest home or substantial assets, you deserve to have your wishes respected and your family protected.

At Daughtry, Woodard, Lawrence & Starling, we understand that talking about end-of-life planning can feel overwhelming or even scary. That’s why our board-certified specialists approach every conversation with genuine compassion and patience. We’ve been helping North Carolina families in Smithfield, Clinton, and throughout Sampson County steer these decisions for decades, and we know that behind every legal document is a real person with real concerns about the people they love.

Our bilingual team ensures that language never becomes a barrier to proper planning. We take the time to explain everything in plain English (or Spanish), answer all your questions, and make sure you feel completely comfortable with every decision. More info about comprehensive estate planning services shows how we tailor our approach to meet each family’s unique needs and circumstances.

The hardest part is often just picking up the phone and scheduling that first appointment. Once you do, you’ll find that estate planning isn’t nearly as complicated or stressful as you might have imagined. In fact, most of our clients leave that first meeting feeling relieved and empowered, knowing they’ve taken a crucial step toward protecting what matters most.

Your legacy extends far beyond bank accounts and property deeds. It’s the love you’ve shared, the values you’ve lived by, and the wisdom you’ve gained over a lifetime. Proper estate planning for seniors ensures that this deeper legacy endures, giving your family not just financial security but also the comfort of knowing they’re honoring your wishes in every decision they make.

Don’t let another day pass wondering if your family will be okay. Take that first step toward peace of mind—for yourself and for the people you love most.