Why Divorce Creates Estate Planning Emergencies

Divorce and estate planning intersect in ways that can devastate your family’s financial future if not handled properly. Here’s what you need to know immediately:

Key Actions Required:

– Update your will within 30 days of divorce finalization

– Change beneficiary designations on all accounts and policies

– Revoke powers of attorney granted to your ex-spouse

– Retitle jointly-owned property

– Create new healthcare directives

Critical Timeline:

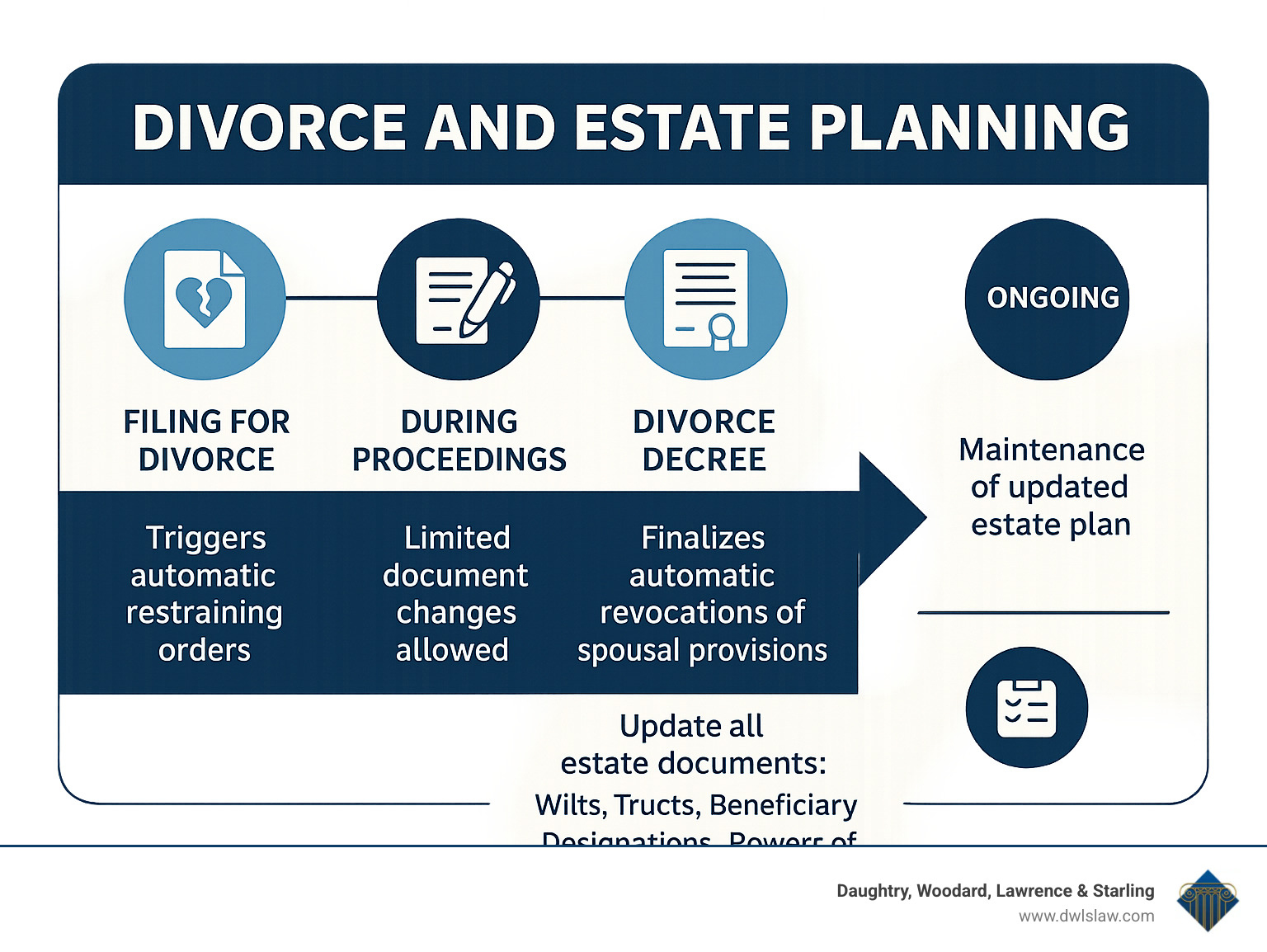

– During divorce: Limited changes allowed due to automatic restraining orders

– After decree: All estate documents need immediate revision

– Failure to act: Ex-spouse may inherit your assets by default

A new divorce action is filed in the United States every 13 seconds, yet most people never consider how this life-changing event affects their estate plan. The emotional toll of divorce often overshadows the urgent need to protect your assets and ensure your wishes are honored.

The stakes are higher than you think. In most states, if you die before updating your estate plan post-divorce, your ex-spouse could still inherit significant assets or make critical medical decisions on your behalf. Even worse, automatic revocation laws vary by state, creating a patchwork of protections that may not cover all your assets.

Gray divorce—divorce after age 50—represents the fastest-growing demographic for divorce in America. These individuals often have substantial assets, complex estate plans, and blended families that make post-divorce planning even more critical.

I’m Kelly K. Daughtry, and with over five decades of legal experience at Daughtry, Woodard, Lawrence & Starling, I’ve guided countless North Carolina families through the complex intersection of divorce and estate planning. Our firm has helped clients steer these challenging transitions while protecting their assets and securing their family’s future.

Know your divorce and estate planning terms:

– divorce attorney smithfield nc

– family attorney nc

– restraining order family law

Why You Must Update Your Estate Plan Post-Divorce

The moment your divorce decree is signed, your estate plan transforms from a protective shield into a potential disaster waiting to happen. Without immediate updates, you’re essentially handing your ex-spouse the keys to decisions you never intended them to make.

The Patchwork Problem of State Laws

Twenty-nine states provide some automatic protection by revoking estate and beneficiary designations that favor an ex-spouse after divorce. But this patchwork of protection is full of dangerous holes that could swallow your family’s financial security.

In North Carolina, the law automatically revokes will provisions favoring your ex-spouse once your divorce is final. Unfortunately, this protection doesn’t extend to many other critical documents. Your life insurance beneficiaries, retirement account designations, and power of attorney documents often remain unchanged.

When “Automatic” Isn’t Automatic Enough

The unintended heir problem is where things get really messy. Most people assume that if their ex-spouse is automatically removed as a beneficiary, their assets will naturally flow to their children or other loved ones. But estate law doesn’t work that way.

Picture this scenario: Your pre-divorce will names your spouse as the primary beneficiary and your sister as the backup. After divorce, automatic revocation removes your spouse from the equation. But now your entire estate—including assets you assumed would go to your children—passes to your sister instead.

The Elective Share Trap

If you die before your divorce is finalized, your spouse remains legally married to you and can claim an elective share of your estate—typically around 30% of your assets. This right exists regardless of what your updated will says.

The Gray Divorce Challenge

The fastest-growing divorce demographic in America is gray divorce—couples divorcing after age 50. If you’re in this group, the stakes are even higher. You likely have substantial retirement accounts, real estate, and complex family structures involving adult children from previous marriages.

Consider a 60-year-old with a $500,000 IRA who forgets to update their beneficiary designations. Their entire retirement savings could flow to an ex-spouse while their children receive nothing.

For detailed guidance on timing your estate plan updates, explore our comprehensive resource on when you should update your will.

Divorce and Estate Planning: Timing and Strategy

When you’re going through a divorce, timing becomes everything—especially when it comes to protecting your estate. The intersection of divorce and estate planning creates a complex web of legal restrictions that can trap you if you don’t understand the rules.

The moment divorce papers are filed, automatic temporary restraining orders (ATROs) kick in, freezing many of your financial options. These orders exist to protect both spouses from having assets hidden or transferred during the proceedings.

What You Can’t Change During Divorce

ATROs typically prevent most financial moves. You can’t change beneficiaries on your life insurance policies, modify who gets your retirement accounts, or transfer assets out of joint accounts. You also can’t sell the house, create new trusts, or cancel insurance policies without permission.

What You Can Still Control

You’re not completely powerless. Most states allow you to execute a new will during divorce proceedings. You can update your healthcare directives and revoke powers of attorney you’ve granted to your spouse.

The ERISA Curveball

Federal ERISA rules throw an extra wrinkle into the mix. Even after your divorce is final and state law automatically revokes your ex-spouse as beneficiary, your 401(k) or pension might not get the memo. ERISA-governed accounts often require you to actively change beneficiaries after divorce.

Smart Pre-Filing Strategy

The savviest approach often involves making estate planning changes before filing for divorce. During this pre-litigation window, you have maximum flexibility to create new wills, establish unfunded trusts, and update your healthcare directives.

For detailed research on estate planning timing during divorce, consult this scientific analysis of estate planning during divorce.

Understanding Automatic Restraining Orders in Divorce

Automatic restraining orders are like financial handcuffs that snap on the moment someone files for divorce. Once these orders take effect, you’re prohibited from making most major financial moves. Divorce and estate planning suddenly becomes a careful dance around legal restrictions.

Despite these restrictions, you can still execute a new will—and you absolutely should. You can also update your healthcare directives and revoke any financial powers of attorney you’ve given your spouse.

Divorce and Estate Planning Checklist Before the Decree

Creating an effective divorce and estate planning strategy during proceedings requires maximizing your options while staying within legal boundaries.

Start with what you can control. Execute a new will that removes your spouse as beneficiary and executor. Update your healthcare powers of attorney and living wills. Revoke any financial powers of attorney you’ve granted your spouse.

For guidance on protecting your finances during divorce proceedings, review our comprehensive guide on protecting finances before the impact of divorce.

Key Documents to Review After the Decree

The moment your divorce decree is signed, the clock starts ticking on one of the most critical phases of divorce and estate planning. Your estate plan needs immediate attention to prevent devastating consequences for your family.

Think of your newly finalized divorce as creating a series of legal gaps that must be filled quickly. When automatic revocations kick in, they don’t just remove your ex-spouse from your documents—they can leave you with no designated beneficiaries, agents, or decision-makers at all.

Your new will should be your first priority. Create a completely fresh document that reflects your current life and wishes. This eliminates any confusion about what was automatically revoked versus what you intended to keep.

Life insurance policies represent one of the most dangerous oversights. While your will provisions may be automatically revoked, many life insurance beneficiary designations remain unchanged. That $500,000 policy could still pay your ex-spouse if you don’t update the forms immediately.

Retirement accounts create their own special headaches. Your 401(k), IRA, and pension plans may not recognize automatic revocations due to federal ERISA rules. Even if state law says your ex-spouse is no longer your beneficiary, the plan administrator might still pay them without updated paperwork.

Powers of attorney need complete replacement, not just revocation. You need trusted people who can handle your finances and make healthcare decisions if something happens to you.

Healthcare directives become especially important after divorce. Who will make medical decisions if you can’t? These documents need updating to reflect your new support system.

| Document Type | Before Divorce | After Divorce | Action Required |

|---|---|---|---|

| Will | Spouse as beneficiary | Automatically revoked | Execute new will |

| Life Insurance | Spouse as beneficiary | May still be valid | Change immediately |

| 401(k)/IRA | Spouse as beneficiary | ERISA may override revocation | Update forms |

| Power of Attorney | Spouse as agent | Usually revoked | Create new document |

| Healthcare Proxy | Spouse as agent | Usually revoked | Name new agent |

| Joint Property | Both names on deed | Varies by state | Retitle as needed |

For comprehensive guidance on navigating these complex post-divorce updates, our detailed resource on what you should do about an estate plan after divorce provides step-by-step guidance.

Wills & Trusts: Starting Fresh

Creating entirely new estate planning documents after divorce eliminates the confusion that comes with automatic revocations. Executor selection becomes particularly important after divorce. Choose someone who won’t be caught in the middle of family conflicts.

Trust restructuring often requires a complete rebuild. Your new individual trust should coordinate with your will through a pour-over strategy—ensuring that any assets not specifically placed in the trust still end up being managed according to your trust’s terms.

Non-Probate Assets: The Silent Danger

The most dangerous oversight in divorce and estate planning often involves assets that never go through probate court. These non-probate assets pass directly to named beneficiaries, bypassing your will entirely.

Retirement account complications create some of the most expensive mistakes. Federal ERISA rules governing employer-sponsored retirement plans don’t always recognize state automatic revocation laws. Your state might say your ex-spouse is no longer your 401(k) beneficiary, but the plan administrator might still pay them if you haven’t filed new beneficiary designation forms.

Powers of Attorney & Healthcare Directives

The end of your marriage creates an immediate need to revoke the decision-making authority you gave your ex-spouse and establish new arrangements for both financial and healthcare decisions.

Agent removal requires active steps. Send written notice to your ex-spouse formally revoking their authority, notify all your financial institutions and healthcare providers about the change, and retrieve any copies of the old documents they might have.

New agent selection deserves careful thought. Your replacement agents need to understand your financial situation, be available when needed, and have no conflicts of interest with your ex-spouse.

Protecting Children, Taxes, and Future Relationships

Post-divorce estate planning extends far beyond updating documents—it requires comprehensive strategies to protect your children’s inheritance, steer tax implications, and plan for potential future relationships.

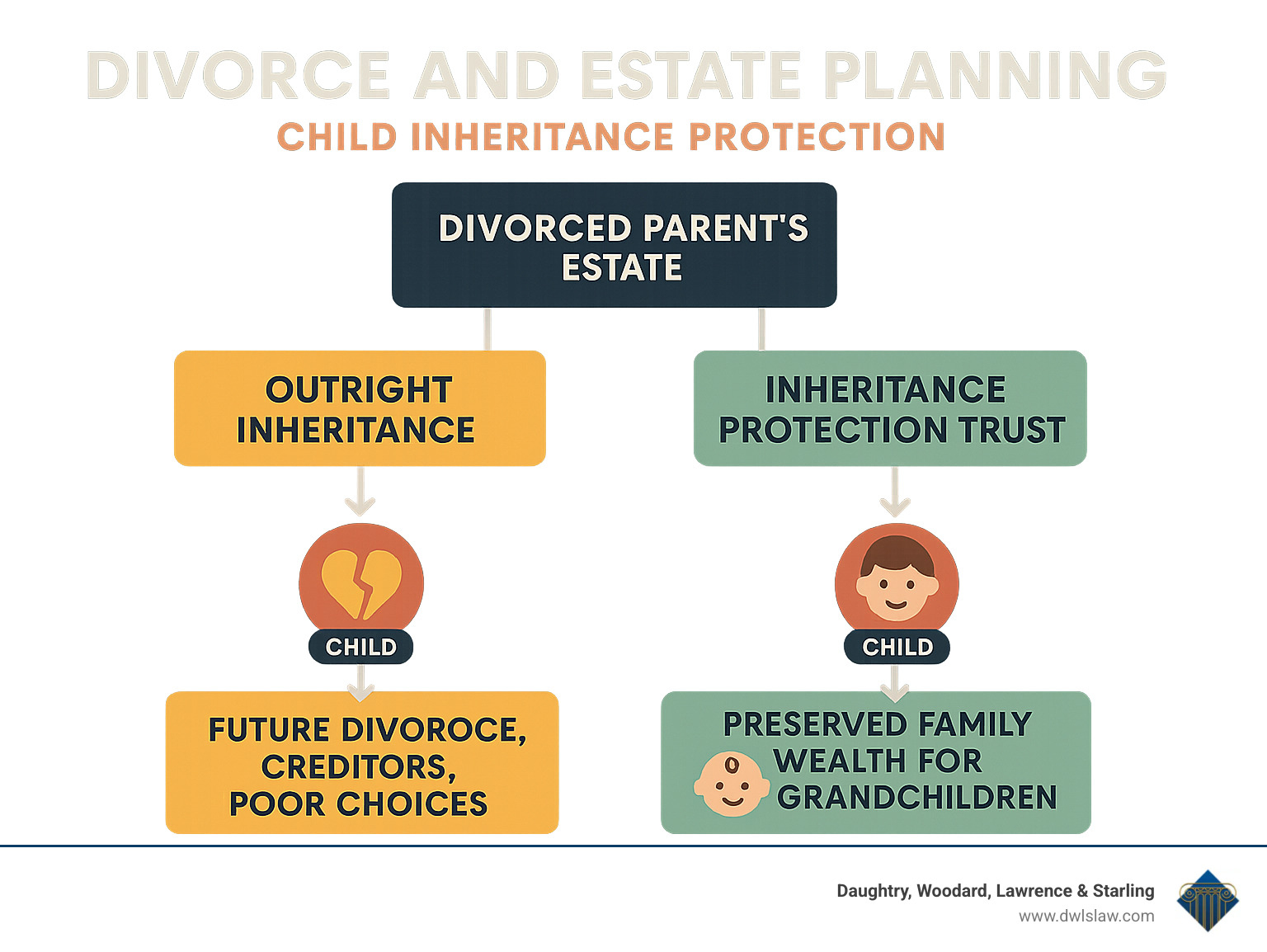

When you’re divorced, your children’s financial future becomes entirely your responsibility to protect. This reality hits many parents hard, especially when they realize their ex-spouse might make decisions they wouldn’t agree with.

Guardianship nominations take on new urgency after divorce. While courts typically favor the surviving biological parent, you can still protect your children by naming standby guardians who would step in if your ex-spouse cannot serve.

Inheritance protection trusts offer powerful benefits that direct inheritances to children cannot match. These trusts shield your children’s inheritance from their own future divorces, protect assets from creditors and poor financial decisions, and provide professional management during their minority.

Many divorce settlements require maintaining life insurance to secure ongoing obligations like alimony or child support. Smart planning coordinates these court-ordered requirements with your broader estate goals.

Federal gift tax rules provide special relief for divorcing couples. You can transfer property tax-free up to one year before divorce, up to two years after divorce, or as part of your settlement.

For specialized guidance on navigating these complex relationships, our resource on estate planning for couples provides detailed strategies for blended families.

Guardianship & Special Needs Considerations

Standby guardian appointments provide crucial backup protection. While courts typically award custody to the surviving biological parent, you can nominate standby guardians who would serve if your ex-spouse is unable, unwilling, or deemed unfit to care for your children.

Special needs trust planning becomes even more critical after divorce. If you have a child with special needs, these trusts preserve government benefit eligibility while providing supplemental support.

Life Insurance & Court-Ordered Obligations

Divorce settlements frequently require life insurance to secure ongoing financial obligations. Alimony security requirements often mandate that the paying spouse maintain life insurance equal to the present value of future payments.

Child support beneficiary planning requires careful attention to ensure funds actually reach your children. When possible, name children as beneficiaries rather than your ex-spouse.

Tax & Asset-Transfer Implications

Basis carryover rules mean that when you receive property in divorce, you typically take the same tax basis your ex-spouse had. This affects your estate planning because highly appreciated property may create large capital gains taxes for your heirs.

Retirement account divisions through QDROs create special rollover opportunities. You typically have 60 days to roll distributed funds into your own IRA, and direct trustee-to-trustee transfers avoid tax withholding.

Conclusion

Going through a divorce is emotionally exhausting, and the last thing you want to think about is updating legal documents. But here’s the reality: divorce and estate planning create an urgent situation that can’t wait until you’re feeling better.

Your estate plan doesn’t automatically fix itself when your divorce is final. While some provisions affecting your ex-spouse may be revoked by law, many critical documents remain unchanged. Your life insurance could still pay out to your former spouse. Your 401(k) might go to someone you never want to see again.

The good news? You’re in control now. For the first time in years, you can design an estate plan that reflects exactly what you want. No more compromising on beneficiaries or worrying about elective share claims.

Start with the basics and work outward. Update your will first—it’s usually the easiest change to make and gives you immediate peace of mind. Then tackle beneficiary designations on retirement accounts and life insurance. Don’t forget powers of attorney and healthcare directives.

Think beyond just removing your ex-spouse. This is your chance to create something better than what you had before. Maybe it’s time to set up trusts to protect your children’s inheritance or finally make sure your sister gets your grandmother’s ring.

You don’t have to figure this out alone. The intersection of divorce and estate planning involves complex legal rules that vary by state and change frequently.

At Daughtry, Woodard, Lawrence & Starling, we’ve helped countless people rebuild their estate plans after divorce. We know you’re dealing with a lot right now, and we make the process as straightforward as possible. Our board-certified specialists understand both family law and estate planning, so we can spot issues that might slip through the cracks.

Your fresh start deserves a fresh estate plan. Don’t let outdated documents from your married life dictate what happens to your family’s future.

For comprehensive guidance on this process, visit our detailed resource on revisiting your estate plan amid divorce.

The sooner you act, the sooner you can stop worrying about “what if” and start enjoying your new independence. You’ve earned it.

Frequently Asked Questions

What happens if I die before my divorce is final?

This scenario creates one of the most challenging situations in divorce and estate planning. If you die while your divorce is still pending, you’re legally married in the eyes of the law—and that means your spouse retains significant rights to your estate.

Your spouse becomes your legal heir again. Even if you’ve been separated for months and have a new will that excludes them, your spouse can claim what’s called an “elective share” of your estate. In most states, this means they’re entitled to about 30% of your assets, regardless of what your will actually says.

Here’s what remains in your spouse’s favor: Any powers of attorney you granted them, executor appointments in your will, and healthcare decision-making authority typically stay valid until the divorce is actually finalized.

The good news is you can execute a new will during divorce proceedings that limits your spouse’s inheritance to the legal minimum required by your state.

Are any beneficiary designations NOT revoked by divorce?

This question reveals one of the most dangerous pitfalls in post-divorce planning. While many people assume divorce automatically cancels all beneficiary designations favoring their ex-spouse, several important exceptions can create costly surprises.

Federal law often trumps state law when it comes to employer-sponsored retirement plans. Even if your state automatically revokes your ex-spouse as beneficiary on your 401(k), federal ERISA rules may not recognize this revocation.

Court-ordered life insurance presents another exception. If your divorce settlement requires you to maintain life insurance with your ex-spouse or children as beneficiaries, you cannot change these designations without violating your divorce decree.

Irrevocable trusts create permanent designations that typically cannot be changed after divorce. If you established irrevocable life insurance trusts naming your spouse as beneficiary, divorce doesn’t automatically remove them.

How soon after filing should I revise my powers of attorney?

The moment you file for divorce, updating your powers of attorney should be your first priority. Unlike many other estate planning documents, you can usually revoke and replace powers of attorney immediately, even while automatic restraining orders limit other changes.

Time is critical because your spouse retains legal authority to make financial and medical decisions for you until you formally revoke their power.

The revocation process requires more than just signing new documents. You need to send written notice to your ex-spouse, notify every bank and financial institution where they had authority, and inform your doctors and healthcare providers about the change.

The key is acting quickly and thoroughly. Divorce and estate planning intersect most dangerously in those first weeks after filing, when emotions run high and important details get overlooked.